Bookkeeping Basics

/

April 22, 2026

April marks the start of Q2 — and if you're a business owner, it's the single most important time of year to get your tax strategy locked in. Not December. Not next quarter. Now.

At ACE CPAs, we work with business owners across industries to transform tax season from a stressful scramble into a confident, strategic win. In this guide, we'll walk you through why Q2 tax planning matters, what moves you should be making right now, and how our upcoming free webinar can help you save $100,000 or more this year.

Most business owners think tax planning is something you do in Q4 or during filing season. But here's what the most profitable businesses know: the best tax-saving decisions happen mid-year, before it's too late to act.

Q2 — April through June — gives you a full six months to course-correct before year-end. That means you still have time to:

Miss this window, and your options shrink dramatically heading into Q3 and Q4. The businesses that save the most aren't necessarily the ones that earn the most — they're the ones that plan the earliest.

Here's a hard truth: if your tax strategy only kicks in when your accountant asks for documents in March, you're already playing catch-up.

Many small business owners unknowingly overpay taxes every year — not because of bad luck, but because of missed opportunities that could have been addressed months earlier. Common examples include:

The good news? Q2 is not too late. In fact, it's exactly the right time to make these adjustments.

At ACE CPAs, our clients who experience the most dramatic tax savings share one thing in common: they engage in proactive, year-round planning rather than reactive filing. Here's what a smart Q2 tax strategy looks like in practice:

If your business has grown significantly in the past year, it may be time to evaluate whether your current entity type still makes sense. An S-Corp election, for example, can reduce self-employment taxes substantially once your net income crosses certain thresholds.

Q2 is a great time to revisit your retirement plan contributions. Whether you're contributing to a SEP-IRA or a Solo 401(k), increasing contributions now reduces your taxable income at year-end while building long-term wealth.

Clean books aren't just about compliance — they're a strategic tool. Reviewing your P&L, balance sheet, and cash flow statements in Q2 gives you a real-time picture of your tax exposure and helps your CPA identify savings opportunities before the year is over.

How and when you take distributions from your business has major tax implications. Working with a CPA to plan distributions correctly can prevent unexpected tax bills and keep more money in your pocket.

The Q2 estimated tax deadline is June 15, 2026. If your business had a stronger-than-expected Q1, you may need to adjust your payment. Underpaying can trigger IRS penalties, while overpaying ties up cash unnecessarily.

At ACE CPAs, we don't just track numbers — we turn your financial data into actionable strategies. Based in Greensboro, NC, and serving business owners nationwide, our team of expert CPAs and bookkeepers specializes in:

✔ Legal tax liability reduction — keeping more of what you earn through proactive planning

✔ Business structure optimization — ensuring your entity type works in your favor

✔ Distribution planning — taking owner compensation in the most tax-efficient way

✔ Full compliance management — no surprises, no penalties, no stress

✔ AI-powered bookkeeping — real-time financial visibility through cutting-edge technology

Our clients consistently report dramatic results — from 35% business growth to tens of thousands saved in taxes annually. As one client put it: "It's like finding hidden money every year."

Ready to take control of your Q2 tax strategy? Join us for a free, live webinar where ACE CPAs' experts will walk you through exactly how high-performing business owners legally minimize their tax burden — and how you can do the same.

Date: April 7, 2026

Time: 7:30 PM EST ]

If you run a small or medium-sized business (SMB), federal and local taxes are among your biggest annual cash outflows. Unfortunately, most SMBs are paying far more than they owe—not because they can’t afford tax bills, but because they confuse basic tax filing with proactive tax planning. This misunderstanding can cost businesses thousands of dollars every year.

In this comprehensive guide, we’ll break down the difference between tax planning vs tax filing, show why SMBs often overpay, and outline legal strategies to reduce your tax burden. Plus, you’ll learn how professional CPA tax strategy can be a game-changer for your business.

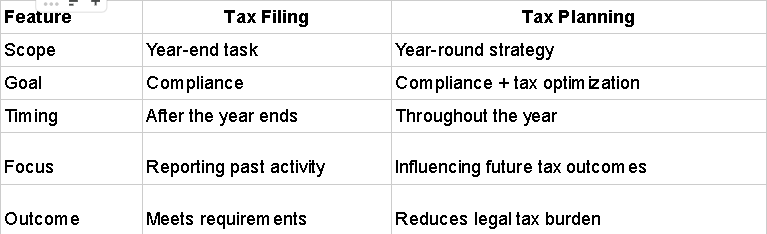

At its core, tax filing is the process of completing and submitting required tax returns to the government—showing your income, expenses, deductions, and calculating what you owe. Most small business owners focus on filing at the end of the year, especially around tax deadlines.

But here’s the problem: tax filing is reactive. You collect receipts, compile records, and fill out forms based on what’s already happened. While filing accurately keeps you compliant, it does nothing to strategically reduce your tax liability.

According to tax professionals, filing alone is often what leads to small businesses overpaying taxes year after year. It treats taxes as a one-time task instead of a year-round financial strategy.

Tax planning for small businesses is a proactive process. It’s thinking strategically about your taxes throughout the year—before income is earned, before expenses are made, and before deductions are tallied. It focuses on legal opportunities to:

Think of it as financial forecasting with tax efficiency as a core goal, rather than an afterthought.

According to IRS-aligned guidelines, tax planning involves analyzing financial performances and decisions throughout the year to ensure that your business pays only what it legally owes—and not a dollar more.

To understand why most SMBs overpay taxes, let’s compare:

In short: filing answers “what happened?” while planning answers “what should happen?”

Understanding why SMBs overpay is the first step toward reducing taxes legally.

Companies often wait until the filing deadline to even think about taxes. By then, opportunities to structure transactions efficiently are gone.

Missed business expenses = missed deductions. Poor record keeping leaks money directly into tax bills.

Sole proprietorships and LLCs taxed as sole proprietors pay self-employment tax on all profits—often resulting in hefty payments. Choosing an S-Corp structure can significantly reduce this.

Some owners avoid claiming deductions they’re legally entitled to, fearing IRS audits, when in fact proper documentation reduces audit risk.

Tax software automates filing but does not offer strategic tax planning. You need expert guidance for optimization.

This leads to confusion and lost deductions, ultimately raising taxable income.

Consider a small business earning $200,000 annually. Without strategic planning:

But a business that:

…can legally save thousands of dollars annually. Experts estimate typical SMBs leave 5–10% of potential savings on the table simply by not planning.

Here are top strategies that distinguish tax planners from mere tax filers:

Switching from sole proprietorship to an S-Corp (where viable) can eliminate up to 15.3% self-employment tax on business profits.

From home office deductions to equipment depreciation, many SMBs fail to take full advantage of tax law benefits that reduce taxable income.

Avoid penalties and better manage cash flow when you plan payments throughout the year.

Contributions to retirement accounts are typically deductible, reducing taxable income while planning for the future.

Accurate records not only ease filing but support deductions and credits, reducing risk during audits.

According to industry analysis, many small businesses are taxed in inefficient ways simply due to reactive tax filing, rather than proactive strategy.

In the U.S., more than 30 million SMBs file as sole proprietorships, subjecting all profits to self-employment tax—costing millions in avoidable taxes.

CPAs with year-round planning practices consistently help clients save more than those offering only tax filing at year-end.

Working with a Certified Public Accountant (CPA) goes beyond simple filing. A CPA who specializes in tax planning will:

The right CPA is not a vendor; they’re a strategic partner that can materially improve cash flow, profitability, and growth.

Accurate planning helps ensure you don’t pay extra. In fact, many eligible deductions go unused without strategic planning.

Rather than facing year-end surprises, your business will have consistent estimates and funds set aside.

You can spend less time worrying about tax compliance and more on innovation and expansion.

If your business is still treating taxes as a once-a-year filing event, it’s time to change that mindset. You don’t want to overpay taxes legally and repeatedly year after year.

Here’s your actionable checklist:

Don’t let another tax season slip by with unnecessary payments.

Partner with expert CPAs who specialize in small business tax planning and strategy.

Visit ACECPAS today to schedule your consultation and start reducing business taxes legally with a customized tax strategy tailored to your SMB.

Exclusive Bonus: Webinar attendees will receive a 20% discount on ACE CPAs services — our way of celebrating Tax Planning Month with business owners who are serious about growth.

Every quarter that goes by without a proactive tax strategy is money you can't get back. The business owners who consistently keep the most aren't lucky — they're prepared.

Whether you're a contractor, a SaaS founder, an e-commerce seller, or a small business owner in any industry, ACE CPAs has the expertise and technology to help you build a tax strategy that actually works.

Q2 is your window. Let's make it count.

.avif)

.avif)